Avoiding Unnecessary Coverage Options

Understanding Car Insurance Coverage Types to Save Money

So, you're trying to save some dough on car insurance, right? Smart move! One of the biggest ways to trim that bill is to ditch coverage you don't really need. But how do you know what's essential and what's just fluff? Let's break down the common types of car insurance and see where you can potentially cut back.

Liability Coverage: The Non-Negotiable

This is the big one. Liability coverage protects you if you're at fault in an accident and cause damage or injuries to someone else. It covers their medical bills, car repairs, and even lost wages. Almost every state requires liability insurance, and for good reason. Skimping on this could leave you financially devastated if you cause a serious accident. Think of it as protecting your assets – your house, your savings, your future earnings. Don't even think about cutting this back to the legal minimum. Consider raising your liability limits to at least $100,000/$300,000 (bodily injury per person/per accident) and $50,000 (property damage). It might cost a little more upfront, but it's worth the peace of mind.

Collision Coverage: Paying for Your Own Mistakes

Collision coverage pays for damage to your car if you're at fault in an accident, or if your car is damaged in a single-car accident (like hitting a tree). The key here is the deductible. This is the amount you pay out-of-pocket before the insurance kicks in. The higher the deductible, the lower your premium. If you have an older car that's not worth much, collision coverage might not be worth it. Think about it: if your car is worth $3,000 and your deductible is $1,000, is it really worth paying for collision coverage? You might be better off putting that money into a savings account to cover potential repairs yourself.

Comprehensive Coverage: Protection from the Unexpected

Comprehensive coverage protects your car from things like theft, vandalism, fire, hail, and hitting an animal. Like collision, it also has a deductible. If you live in an area prone to severe weather or car theft, comprehensive coverage might be a good idea. But again, consider the value of your car. If your car is older and not worth much, you might be better off skipping this coverage.

Identifying Unnecessary Car Insurance Coverage Options for Savings

Now let's drill down into the areas where you can often find wiggle room to save money.

Rental Car Reimbursement: Do You Really Need It?

Rental car reimbursement covers the cost of a rental car while your car is being repaired after an accident. It sounds good in theory, but think about how often you actually need a rental car. If you have another car you can use, or if you can easily get by with public transportation or ridesharing, you might not need this coverage. Also, check your credit card benefits. Many credit cards offer rental car insurance as a perk, which could make this coverage redundant.

Roadside Assistance: Are You Already Covered?

Roadside assistance covers things like towing, jump starts, and tire changes. Many car insurance companies offer this as an add-on, but you might already be covered through another source. Do you have AAA membership? Does your car manufacturer offer roadside assistance? Check your existing benefits before adding this to your car insurance policy. Sometimes, a simple AAA membership is cheaper and offers more comprehensive coverage.

Medical Payments Coverage (MedPay) and Personal Injury Protection (PIP): Knowing the Difference

MedPay and PIP cover medical expenses for you and your passengers, regardless of who's at fault in an accident. PIP also covers lost wages in some states. The necessity of these coverages depends on your health insurance situation. If you have good health insurance, you might not need MedPay or PIP. However, if you have a high deductible or co-pay, or if you don't have health insurance, these coverages could be beneficial. Also, some states require PIP, so make sure you understand the laws in your state.

Uninsured/Underinsured Motorist Coverage: Protecting Yourself from Negligent Drivers

This coverage protects you if you're hit by an uninsured or underinsured driver. It covers your medical bills, car repairs, and lost wages. While it's not always legally required, it's highly recommended. The reality is that many drivers on the road don't have adequate insurance, and if you're hit by one of them, you could be left with significant expenses. This is one area where you probably don't want to skimp.

Specific Product Recommendations and Comparisons for Cost-Effective Car Insurance Add-ons

Okay, let's get into some specific products and scenarios to help you make informed decisions about add-ons. Remember, these are just examples, and you should always compare quotes from multiple insurers.

OBD-II Connected Devices for Usage-Based Insurance (UBI)

Several companies offer devices that plug into your car's OBD-II port (usually located under the steering wheel) to track your driving habits. This data is then used to calculate your insurance premium. If you're a safe driver, you could save a significant amount of money.

Product Examples:

- Progressive Snapshot: One of the most well-known UBI programs. It tracks things like hard braking, rapid acceleration, and nighttime driving. Good for drivers who consistently drive safely. Potential savings: Up to 30%. Cost: Free device.

- Allstate Drivewise: Similar to Snapshot, but also includes mileage tracking. Good for low-mileage drivers. Potential savings: Up to 25%. Cost: Free app or device.

- State Farm Drive Safe & Save: Tracks similar data to Progressive and Allstate. Potential savings: Up to 50% (depending on driving habits). Cost: Free app.

Usage Scenarios:

- Scenario 1: Sarah is a cautious driver who primarily uses her car for commuting to work and running errands during the day. She rarely drives at night and avoids aggressive driving maneuvers. She would likely benefit from using a UBI program like Progressive Snapshot or Allstate Drivewise.

- Scenario 2: Mark is a college student who only drives his car occasionally to visit family on weekends. He drives responsibly but occasionally drives late at night. He might benefit from State Farm Drive Safe & Save, but should carefully consider the impact of nighttime driving on his potential savings.

- Scenario 3: Emily is a sales representative who drives extensively for work and often drives at night. She frequently encounters heavy traffic and may need to brake hard or accelerate quickly. She is unlikely to benefit from a UBI program and may even see her rates increase.

Product Comparison:

| Feature | Progressive Snapshot | Allstate Drivewise | State Farm Drive Safe & Save |

|---|---|---|---|

| Data Tracked | Hard braking, rapid acceleration, nighttime driving | Hard braking, rapid acceleration, nighttime driving, mileage | Hard braking, rapid acceleration, cornering, speeding, distraction |

| Potential Savings | Up to 30% | Up to 25% | Up to 50% |

| Cost | Free device | Free app or device | Free app |

| Device Type | OBD-II device | App or OBD-II device | App |

| Privacy Considerations | Data is used to determine your premium | Data is used to determine your premium | Data is used to determine your premium |

Dash Cams with Accident Recording and Reporting Features

Dash cams are becoming increasingly popular, not just for recording accidents, but also for potentially lowering your insurance premiums. Some insurers offer discounts for using dash cams that provide detailed accident data.

Product Examples:

- Garmin Dash Cam 67W: High-quality video, wide viewing angle, automatic incident detection. Price: Around $250.

- Thinkware F200 Pro: Reliable performance, parking mode recording, easy to use. Price: Around $150.

- Vantrue N2 Pro: Dual-channel recording (front and interior), night vision, loop recording. Price: Around $200.

Usage Scenarios:

- Scenario 1: John lives in a busy city with a high risk of accidents. He wants a dash cam that can provide clear video evidence in case of an accident. The Garmin Dash Cam 67W would be a good choice.

- Scenario 2: Lisa wants a dash cam primarily for parking mode recording to protect her car from vandalism or hit-and-run incidents. The Thinkware F200 Pro would be a suitable option.

- Scenario 3: David drives for a ridesharing service and wants a dash cam that can record both the road ahead and the interior of his car. The Vantrue N2 Pro would be the best choice.

Product Comparison:

| Feature | Garmin Dash Cam 67W | Thinkware F200 Pro | Vantrue N2 Pro |

|---|---|---|---|

| Video Quality | 1440p | 1080p | 1080p (front), 1080p (interior) |

| Viewing Angle | 180 degrees | 140 degrees | 170 degrees (front), 140 degrees (interior) |

| Parking Mode | Yes (requires hardwiring kit) | Yes | Yes |

| Price (approx.) | $250 | $150 | $200 |

| Insurance Discount Potential | Varies by insurer; check with your provider | Varies by insurer; check with your provider | Varies by insurer; check with your provider |

Anti-Theft Devices and Vehicle Recovery Systems

Installing anti-theft devices can sometimes qualify you for a discount on your comprehensive coverage. Vehicle recovery systems like LoJack can also offer peace of mind and potential savings.

Product Examples:

- LoJack: A widely used vehicle recovery system that helps law enforcement locate and recover stolen vehicles. Cost: Approximately $700-$1000 (including installation).

- Viper 5706V: A car alarm system with remote start, keyless entry, and smartphone control. Cost: Approximately $300-$500 (including installation).

- Ravelco Anti-Theft Device: A unique system that prevents the car from being started without a specific plug. Highly effective, but more expensive. Cost: Approximately $500-$700 (including installation).

Usage Scenarios:

- Scenario 1: Maria lives in an area with a high rate of car theft and wants the best possible chance of recovering her vehicle if it's stolen. LoJack is a suitable option.

- Scenario 2: Tom wants a car alarm system that provides both security and convenience features like remote start. The Viper 5706V would be a good choice.

- Scenario 3: Carlos wants the most effective anti-theft device available, regardless of cost. The Ravelco Anti-Theft Device is a highly secure option.

Product Comparison:

| Feature | LoJack | Viper 5706V | Ravelco Anti-Theft Device |

|---|---|---|---|

| Primary Function | Vehicle recovery | Car alarm system | Prevents vehicle from being started |

| Effectiveness | High (vehicle recovery rate) | Moderate (deters theft) | Very High (prevents theft) |

| Cost (approx.) | $700-$1000 (including installation) | $300-$500 (including installation) | $500-$700 (including installation) |

| Insurance Discount Potential | Yes (check with your insurer) | Yes (check with your insurer) | Yes (check with your insurer) |

| Additional Features | GPS tracking, stolen vehicle recovery assistance | Remote start, keyless entry, smartphone control | Requires a unique plug to start the car |

Adjusting Deductibles for Cheaper Car Insurance Premiums

One of the simplest ways to lower your car insurance premium is to increase your deductible. But it's a balancing act. You need to be comfortable paying that deductible out-of-pocket if you have an accident.

Finding the Right Deductible Level for Your Budget

Think about how much you can realistically afford to pay out-of-pocket in case of an accident. Could you easily cover a $500 deductible? A $1,000 deductible? A $2,000 deductible? The higher the deductible, the lower your premium will be, but you need to be prepared to pay that amount if you need to make a claim.

The Impact of Deductible Changes on Car Insurance Costs

Let's say you currently have a $250 deductible for both collision and comprehensive coverage. Increasing that to $500 might save you 5-10% on your premium. Increasing it to $1,000 could save you 15-20%. Get quotes from your insurer with different deductible levels to see how much you can save. It's a good idea to put the difference in savings into an emergency fund to cover the higher deductible if needed.

Bundling Car Insurance with Other Policies for Maximum Savings

Many insurance companies offer discounts if you bundle your car insurance with other policies, such as homeowners insurance or renters insurance. This is often one of the easiest ways to save money on insurance.

Combining Car Insurance with Homeowners or Renters Insurance

Bundling your car insurance with homeowners or renters insurance can often save you 10-20% on your overall insurance costs. It's worth getting quotes from multiple insurers to see which one offers the best bundling discount. Even if one insurer offers a slightly lower premium for car insurance alone, the bundling discount might make another insurer the better choice overall.

Exploring Other Bundling Opportunities for Additional Discounts

Some insurers also offer discounts for bundling car insurance with other types of insurance, such as life insurance or umbrella insurance. It's worth exploring all your options to see how much you can save. Just make sure you're not sacrificing coverage quality for the sake of a discount.

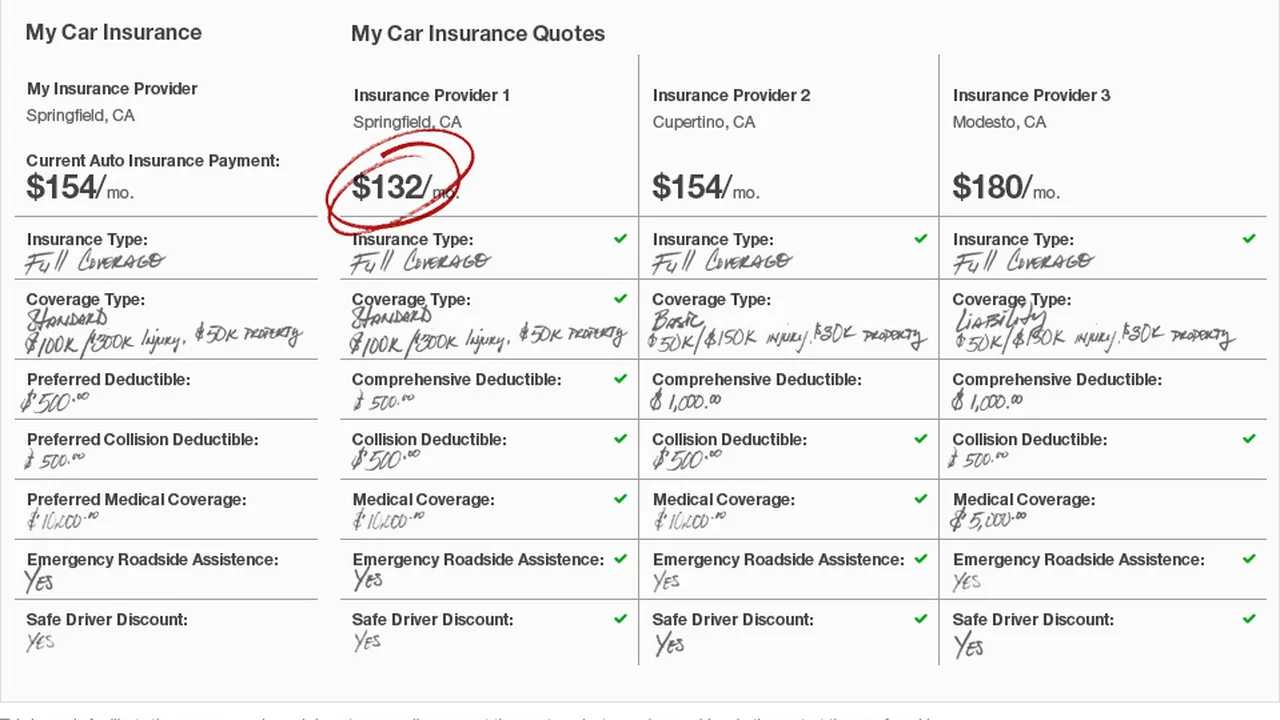

Shopping Around and Comparing Car Insurance Quotes Regularly

This is the golden rule of saving money on car insurance. Don't just stick with the same insurer year after year. Shop around and compare quotes from multiple insurers at least once a year, or whenever you experience a major life change (like moving or buying a new car).

Using Online Comparison Tools to Find the Best Deals

There are many online comparison tools that can help you quickly compare quotes from multiple insurers. Some popular options include:

- The Zebra: Compares quotes from multiple insurers and provides personalized recommendations.

- NerdWallet: Offers a car insurance comparison tool and provides helpful articles and resources.

- QuoteWizard: Compares quotes from multiple insurers and offers a variety of insurance products.

Understanding the Factors That Influence Car Insurance Rates

Car insurance rates are influenced by a variety of factors, including your age, driving record, location, type of car, and coverage choices. Understanding these factors can help you make informed decisions about your insurance coverage.

Negotiating with Your Current Insurer for a Lower Rate

Don't be afraid to negotiate with your current insurer. If you find a lower quote from another insurer, let your current insurer know. They might be willing to match the lower quote to keep your business. It's always worth a try!

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)